Many credit card users assume that converting their outstanding balance into EMIs will reduce the interest rate they pay. While EMI conversion can help make repayment more structured, the reality is that the interest rate remains the same for both regular outstanding amounts and EMI conversions. The only difference is in the payment method, not the cost of borrowing.

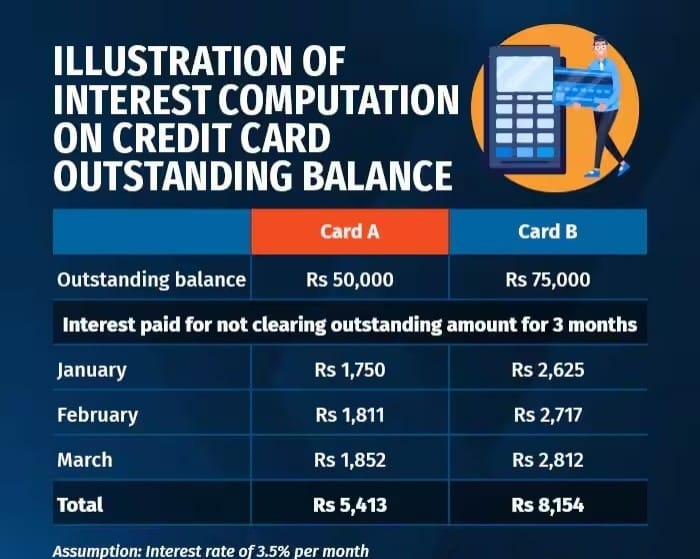

Credit cards typically offer a grace period of around twenty one days after the billing date. If you pay your full balance within this period, you avoid any interest charges. However, once you cross that due date without clearing the full amount, interest is charged on the daily outstanding balance. What makes this more expensive is that any new purchase you make after the due date also starts attracting interest from the very first day, as long as there is an unpaid balance.

When you choose to convert your dues into EMIs, you are essentially breaking down your repayment into smaller monthly instalments. This can make the repayment process easier to manage, especially for large purchases or significant dues. However, the interest rate applied to this EMI amount is usually the same as what you would have paid on your regular outstanding balance. This is because the bank calculates interest on the average daily balance, and unless you clear a portion of it, the cost does not change. Therefore, if you have surplus funds at any point, it is wise to make part-payments to bring down the principal and reduce overall interest costs.

Many shoppers are also attracted by interest-free EMI offers on credit cards, especially during sales or festive seasons. These offers are not truly interest-free in the purest sense. In most cases, the seller covers the interest cost on behalf of the buyer. This can sometimes be reflected in a higher product price compared to other purchase methods. By checking the price across different platforms or payment options, you may find that paying upfront without opting for EMI could save you money, even without a visible interest charge.

The principles of interest and repayment remain the same across credit products, whether it is for purchasing electronics, financing education, or taking a home loan. For instance, a borrower who requires only a small percentage of a property’s price through a home loan can opt for a shorter tenure, such as five years, provided their repayment capacity supports it. Similarly, in education loans, smaller amounts often do not require collateral, while larger loans may require security in the form of real estate or financial assets.

The key takeaway for credit card users is that managing debt efficiently is more about timing and discipline than about the repayment format. Always aim to pay off your full balance within the interest-free period whenever possible. If conversion to EMI makes sense for your budgeting, use it as a repayment strategy, but do not expect it to lower the actual interest rate. By understanding these details, you can use credit cards as a financial tool rather than letting them become a debt trap.

For more practical tips on debt management, credit card strategies, and smart borrowing, follow You Finance on Instagram and Facebook.